The Complete Guide to Flipping Land for Profit

This guide covers every step of land flipping from sourcing underpriced parcels and securing funding to marketing effectively, negotiating deals, and closing with precision. Backed by real-world ROI examples, decision-flow infographics, and downloadable templates, readers will gain the confidence and tools needed to execute their first flip and build a repeatable, scalable flipping business.

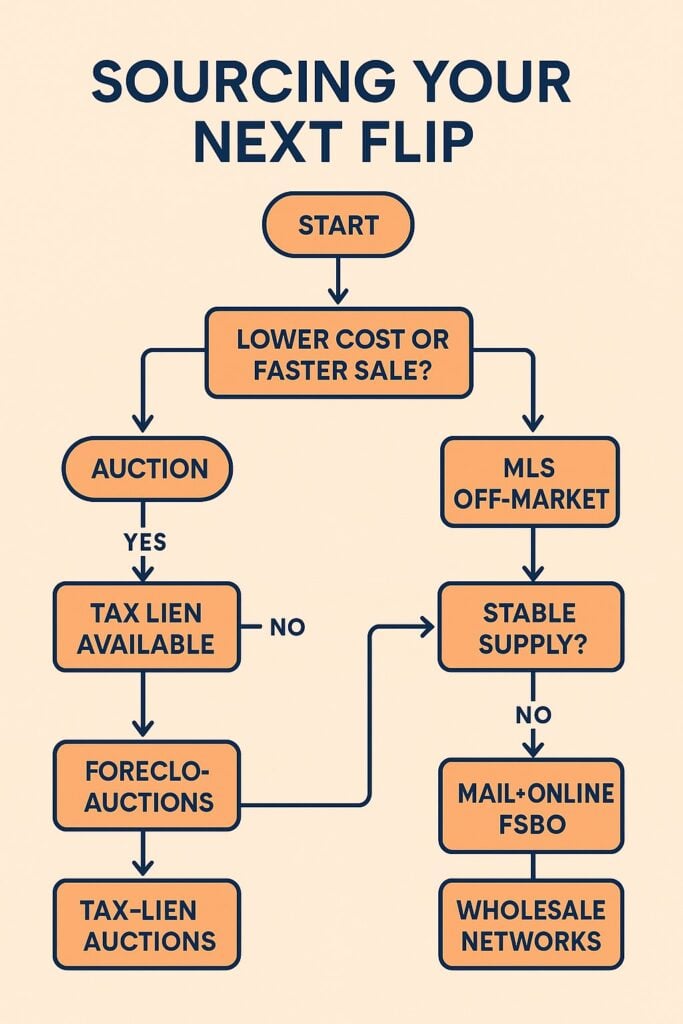

How do I find the best land deals to flip?

To find the best land deals to flip, explore multiple sourcing channels, such as tax-lien auctions, MLS off-market pockets, and wholesale networks. Set up targeted alerts and weigh each method’s cost-to-speed trade-off using a decision-flow approach.

Begin at county tax-lien auction portals to spot deeply discounted properties. Compare the required upfront capital and typical turnaround time. Next work with local agents to gain access to pocket listings on MLS and set up custom alerts for motivated sellers. Join wholesale land networks and online marketplaces to uncover bulk-deal opportunities. Use the decision-flow infographic below to determine whether you need lower acquisition costs or faster deal cycles based on your capital and timeline constraints.

How do I source off-market land deals on MLS?

To source off-market land deals on MLS, you should network with top-producing agents, request access to pocket listings, and set custom search alerts for properties that meet your criteria.

Identify agents specializing in vacant land or distressed sales and build relationships by attending local real-estate meetups. Ask them to notify you of upcoming pocket listings that are not publicly advertised. Log into your MLS account and create saved searches filtering for days-on-market over 90, pre-foreclosure status, or expired listings. Receive email alerts instantly when new matches appear. Reviewing these hidden opportunities can yield 10 to 20 percent below-market deals before they hit the general market.

What strategies work best at tax-lien and foreclosure auctions?

To succeed at tax-lien and foreclosure auctions, you should register early, complete thorough due diligence on title and property conditions, and set strict bid limits based on your exit strategy.

Register online or in-person at the county auction site weeks before the event. Obtain parcel details and perform a preliminary title search for liens and easements. Visit the property if possible to assess access and condition. Calculate your maximum bid by subtracting estimated closing costs, remediation expenses, and desired profit margin from probable resale value. During the auction, stick to your limit to avoid overpaying. Winning at 60 to 70 percent of market value creates room for renovations, marketing, and profit.

How do I finance a land flip?

To finance a land flip, you should compare options such as all-cash purchases, hard-money loans, private-money lenders, and seller financing, then select the option that minimizes your cost of capital and aligns with your project timeline.

📘 Get Your FREE Land Investing Strategy Guide

Discover how savvy investors build passive income with vacant land.

All-cash deals close fastest and avoid interest costs but tie up your capital. Hard-money loans provide quick funding at higher interest rates and short terms, ideal for rapid flips. Private-money lenders often offer more flexible terms and may consider your track record. Seller financing lets you negotiate down payments and amortization schedules directly with the seller, reducing bank fees and speeding closing.

Balancing cost and speed is essential. For example, a $100,000 land parcel financed with a hard-money loan at 12 percent interest and a 6-month term incurs $6,000 in interest, while seller financing at 8 percent over one year costs $8,000 but spreads payments more manageably.

When does seller financing (owner carry) make sense?

Seller financing makes sense when the seller is motivated to receive steady income, you need to minimize bank approval delays, and you can negotiate favorable terms such as lower down payments or longer amortization.

Ask the seller to carry 70 to 90 percent of the purchase price, with you paying interest-only monthly payments or a fully amortized schedule. Negotiate interest rates 1 to 3 percent above prime to benefit both parties. Include balloon-payment options after three to five years if you plan to refinance or sell quickly. Ensure the purchase agreement includes a lien position clause so you understand your collateral priority.

This structure allows you to preserve cash for closing costs and improvements, while the seller enjoys predictable returns without managing the land.

What are the pros and cons of hard-money loans?

Hard-money loans provide rapid funding based on collateral value rather than credit history, making them ideal for investors who need to close deals quickly, but they carry higher interest rates and origination fees.

Rates typically range from 8 to 15 percent, with points of 2 to 4 percent at origination. Loan terms are short, often six to twelve months forcing a quick flip or refinance. Approval can occur in days since underwriting focuses on the land’s after-repair value. However, interest costs and fees eat into profit margins, and lenders may require a lower loan-to-value ratio, such as 60 percent.

Use hard-money only when speed outweighs cost. For a $100,000 purchase, expect $2,000 to $4,000 in origination fees plus $6,000 to $12,000 in interest for a one-year term. Ensure your flip plan covers these expenses.

What due diligence must I perform before flipping?

To perform due diligence before flipping, you should order a title search, verify zoning and land-use restrictions, commission a Phase 1 environmental audit, and hire a surveyor to confirm boundaries and easements.

Begin by ordering a title report from a reputable title company to uncover liens, mortgages, or judgments against the property. Next check local zoning maps and land-use ordinances with the planning department to confirm that your intended use is permitted. Commission a Phase 1 environmental site assessment to identify potential contamination from prior uses. Finally engage a licensed surveyor to verify parcel lines and reveal any encroachments or easements that could affect resale value.

Skipping these steps can expose you to costly surprises after closing. A title search typically costs $200 to $400. A Phase 1 audit runs $800 to $1 200. Surveys vary by acreage but average $100 to $200 per acre. Budget these into your deal analysis.

How do I uncover hidden liens and encumbrances?

To uncover hidden liens and encumbrances, you should search county recorder records for recorded mortgages, judgments, and mechanics’ liens, and request a current title commitment outlining exceptions.

Visit the county recorder or use its online portal to pull chains of title back at least 20 years. Look for recorded liens, easements, or right-of-way grants. Order a title commitment from a title insurer that will list exceptions and survey matters. Review exceptions with the insurer to determine if endorsements can cover title defects.

What environmental or zoning risks should I watch for?

To identify environmental or zoning risks, you should review the Phase 1 audit report for recognized environmental conditions, consult FEMA flood maps, and verify local conditional-use requirements.

Your Phase 1 audit will flag known contamination, proximity to landfills, or underground storage tanks. Compare parcel coordinates against FEMA’s flood-zone maps to determine flood insurance needs. Check county land-use codes for special permits required for subdivisions or commercial uses. Addressing these issues up front avoids remediation costs and permit delays.

How do I market and list my flip for maximum exposure?

To market and list your flip for maximum exposure, you should craft professional FSBO listings, deploy targeted digital ads, offer virtual tours, and consider turnkey listing services for wider reach.

Start by writing a compelling FSBO headline that highlights acreage, location, and unique features. Capture high-resolution aerial and ground photos. Set up Facebook and Google Search campaigns targeting buyers in your region using geo-fencing. Create a 360-degree virtual tour to engage remote prospects. If you prefer full service, partner with a listing platform that handles photography, syndication, and lead management.

An effective mixed-channel approach can halve days on market and boost sale price by 5 to 10 percent.

What digital marketing channels drive the most qualified leads?

To drive qualified leads, you should use Facebook custom audiences for demographic targeting, Google Search ads for high-intent keywords, and LinkedIn for commercial land prospects.

On Facebook, set up look-alike audiences based on past buyer lists. On Google bid on keywords like “vacant land for sale cheap” and “rural land flips.” Utilize ad extensions to showcase acreage and price. On LinkedIn promote to investors or developers in relevant industries. Track cost-per-lead and adjust budgets weekly.

How do I craft FSBO listings that convert?

To craft FSBO listings that convert, you should write benefit-focused headlines, include a photo checklist covering all angles, and end with a clear call to action to schedule a site visit.

Use a headline such as “20 Acres with Highway Frontage and Buyer Financing.” Include at least ten photos: aerial, road access, boundaries, utilities, and sunsets. Close with “Call now to tour this investment opportunity.” Offering owner-carry financing and providing sample payment terms can further entice buyers.

How do I negotiate deals to boost my margin?

To negotiate deals that boost margin, you should open with an anchor offer well below market, use data to justify your price, and include contract contingencies that protect your exit strategy.

Begin with a written offer at 60 to 70 percent of your estimated after-repair value. Include a comparative market analysis showing recent nearby sales. Add contingencies for due diligence, financing, and assignment rights if you plan to wholesale. Remain polite but firm, and be ready to walk away if the seller refuses key terms.

Structuring offers this way often encourages motivated sellers to compromise, preserving margin for rehab, marketing, and profit.

What anchor offers should I use to get under market value?

To set an anchor offer that lands under market value, you should calculate your maximum allowable offer based on resale value minus costs and profit, then subtract an additional 10 percent buffer.

If the property’s ARV is $100,000 and rehab plus fees total $20,000 and desired profit is $10,000, your MAO is $70,000. Offer $63,000 initially. Justify the lower price with needed repairs, title and survey costs, and holding expenses. This transparent approach often leads to mid-point negotiations around $68,000.

How do I structure option or assignment contracts?

To structure option or assignment contracts, you should draft an option agreement granting you the right to purchase at a set price, include a non-refundable deposit, and add clear assignment permission.

In your option agreement state the purchase price, term length, and deposit amount. Specify that you may assign your rights to another party. Use a standard memorandum of option for public record to block resale. For assignments, include a clause requiring the assignee to close under original terms, protecting your profit margin without additional risk.

What closing process ensures a smooth flip?

To ensure a smooth flip closing, you should choose the right closing method, prepare escrow instructions early, and review closing costs and prorations with your title company well before the closing date.

Decide between self-closing for lower fees or using a title company for full-service escrow. Submit escrow instructions including payoff amounts, deed type, and wire details at least one week ahead. Request a preliminary closing statement showing prorated taxes, title insurance premiums, recording fees, and any seller credits. Verify all documents and funds are ready to avoid last-minute delays.

A clear closing process prevents extended hold times and additional carrying costs.

When should I self-close versus use a title company?

To decide between self-closing and a title company, you should compare cost savings against risk tolerance for handling documents and wiring funds.

Self-closing can save 10 to 20 percent on escrow fees if you are comfortable preparing documents and managing escrow yourself. Using a title company adds convenience, legal oversight, and escrow services that reduce risk of errors or wire fraud. Newer investors may prefer the security of a title company despite higher cost.

How do I calculate and minimize closing costs?

To calculate closing costs, you should request a Good Faith Estimate detailing title insurance, recording fees, escrow fees, and prorated taxes, and shop for the best title-insurance rate discounts.

Gather GFE line items from multiple title insurers and ask for lender and owner policy bundle discounts. Confirm local recording fees per page and parcel. Review prorations for property taxes and HOA fees. Negotiating to split certain fees with the buyer can reduce your out-of-pocket expenses by 20 to 30 percent.

How do I scale and repeat my land-flipping business?

To scale your land-flipping business, you should document processes in playbooks, automate lead generation, partner with reliable contractors, and consider forming joint ventures with investors or agents.

Start by creating standard operating procedures for sourcing, due diligence, financing, and marketing. Use CRM software to automate follow-ups and nurture leads. Build relationships with surveyors, title companies, and local crews for reliable service. Invite passive investors into joint-venture deals using profit-sharing agreements. Aim to complete one flip in 90 days and reinvest profits to fund additional projects.

A systematic approach can grow your flips from one deal per year to five or more.

What metrics should I track for each flip?

To track flip performance, you should monitor purchase price, total holding costs, marketing expenses, sell price, days on market, and net profit margin.

Maintain a deal tracker spreadsheet logging all acquisition and renovation costs, financing fees, and sale proceeds. Calculate return on investment and annualized yield. Track days from contract to close and days on market to optimize timelines. Use these metrics to refine offer strategies and budget accuracy.

How do I build a team or JV partnerships?

To build a team or joint-venture partnerships, you should identify complementary skill sets, draft clear partnership agreements, and define profit splits and decision-making roles.

Seek partners offering capital, expertise, or access to deals. Outline roles in a written agreement specifying capital contributions, preferred returns, and equity splits. Include decision-making protocols and dispute-resolution clauses. Regularly review performance and adjust partnerships to maintain alignment and momentum.

Mini FAQ

What is the typical profit margin on a land flip?

Most flips yield 15 to 30 percent net profit after all costs and fees, depending on deal structure and market conditions.

Can I wholesale land without closing?

Yes, you can assign an option contract to another buyer for an assignment fee, avoiding a full purchase and resale.

How long does a typical land flip take?

A streamlined flip can close in 60 to 90 days; more complex deals or entitlement flips may take 6 to 12 months.